Hey y’all,

So I’m gonna talk about the Fed again.

Sorry, I know I’m a bit of a broken record this week. But I’m really concerned that the stock market is setting up for a huge disappointment next week.

And headlines like this aren’t putting my mind at ease:

According to CME FedWatch, traders are now pricing in a 43% chance of a 50 basis points rate cut next week — up from 28% just yesterday.

This strikes me as irrational.

Chairman Powell, whatever his strengths and his weaknesses, has been anything but quick on the trigger.

Many criticize him for waiting too long to raise rates. And while you could argue that such criticism will pressure him to lower them more quickly, I don’t necessarily agree…

I think we’re looking at a Fed Chairman defined by caution. He’s concerned about his legacy, and he knows that “slow and steady” is probably the safest way to proceed.

But there’s another thing most people are forgetting.

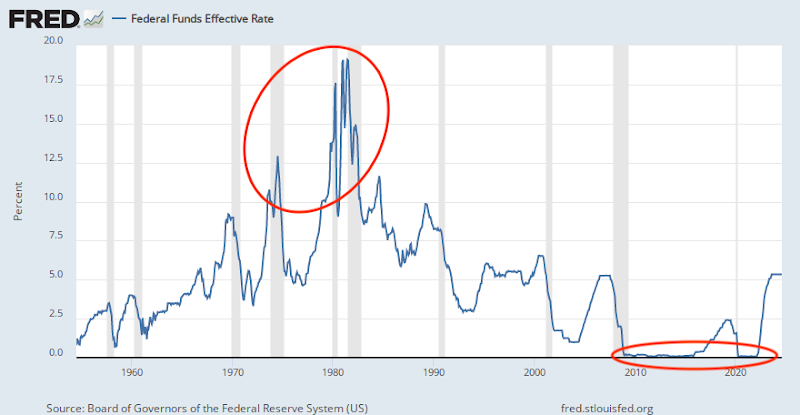

Because we had at or near-zero interest rates for many years before the COVID-19 pandemic, most people believe that a return to those levels is “a return to normal.”

Nothing. Nothing could be further from true.

Put bluntly, a near-0% interest rate is as much of an outlier as the 10+% rates we saw in the 70s and 80s.

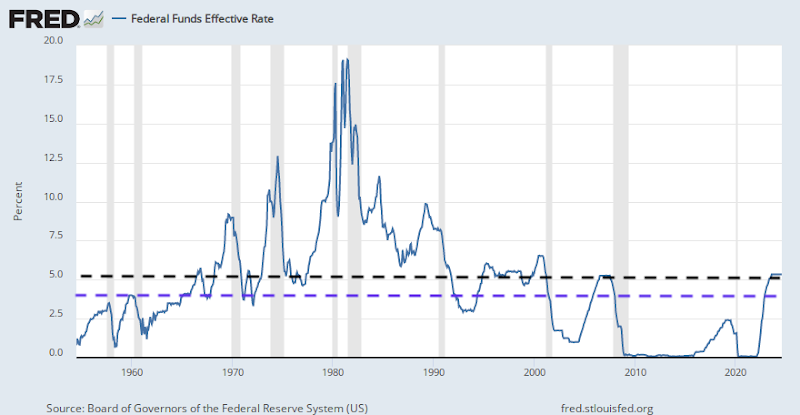

Upon closer inspection, the “average” interest rate since 1971 has been 5.42%, which is right in line with our current rate threshold.

But even if you remove the sky-high interest rates from the equation, and just look at the last 30ish years (since 1990) the average rate is approximately 3.65%.

Represented on the chart below (1970 average in black, 1990 average in violet), you can see we don’t have that far to go to return to “normal”…

So the question then becomes, is Powell trying to restore a pre-COVID reality? Or is he trying to return the whole economy to “neutral?”

The decade of uninterrupted bull markets we always talk about in the 2010s was also just a very slow and drawn-out economic recovery from the 2008 crisis.

And the fact that this recovery was brought to an end not by natural causes, but by a black swan pandemic, has warped our perception of what “normal” really is.

Powell will have to decide if the way forward takes us back closer to zero or more in the 3-4% range. If I had to bet, I’d bet on the latter.

But I think most investors are expecting the former.

The resulting disappointment could create temporarily deflated hopes in the markets, and cause us to see some extended corrections.

Those could start as soon as Wednesday next week.

I’m not a bear by any means. I think the markets have lots of room for upward mobility left.

But I do think a correction and a reorientation needs to happen. We need to let some air out of the balloon, and then refocus on what actually matters in the markets.

We hyper-focus on the Fed as the sign of whether the economy and the stock market is healthy…

But we ignore the more obvious signs.

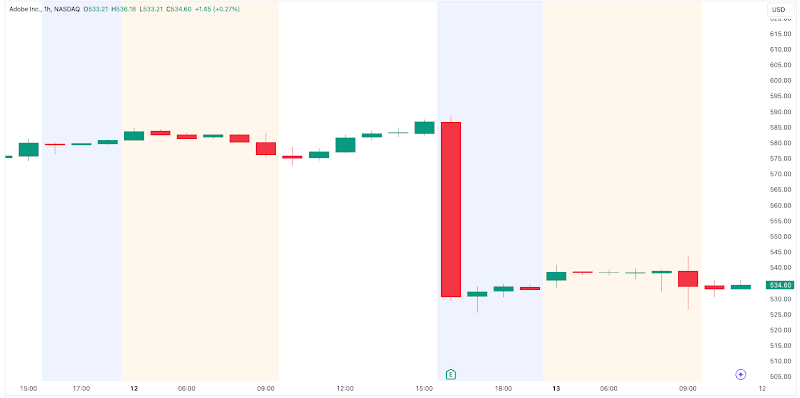

ADBE stock is a good example — a double beat on earnings today, but lowered future guidance caused a massive stock loss of nearly 10%.

NVDA a few weeks ago was another great example of this.

Investors can’t see the forest for the trees right now — they’re so forward-focused that they don’t see the dozens of thriving companies right in front of their eyes.

So I think we need to correct that a little bit, and reorient towards the present.

Then, it’s off to the races…

But as long as investors hang their hopes on the Fed as the weathervane of the stock market, I think there’s going to be lots of disappointment and hiccups along the way.

Hope there are no hiccups for your weekend plans! Enjoy the time…

To your Prosperity,

— Stephen Ground

Editor in Chief, ProsperityPub

P.S. The one good thing next week’s Fed meeting could bring to the market is volatility. And Nate Tucci has big plans to harness that volatility when it hits!