The last time the FOMC hiked 75 basis points, they put me out of a job.

Fresh out of college, I was an entry-level loan processor for a mortgage company. But Alan Greenspan got a little nervous about rapid economic growth driving inflation, so he put the kibosh on the refi pipeline.

When I started, we processed 50 loans a day. Within 6 months, that fount of loan processing fees dried up and, just like that, me and 80 of my newest friends were walking across the parking lot, cardboard boxes in hand.

It worked out though. Within a couple of months, I sold my Honda Accord, packed up my belongings (it fit in the trunk of my friend’s car), and headed to Chicago to sleep on a Fraternity brother’s couch. The plan was to work my way onto the floor of the Chicago Board of Trade.

Ah, those were the days…

This time around, it’s not about anticipating inflation. The Fed is playing catch up.

And growth has nothing to do with it…

The Birth of My Hate/Hate Relationship With The Fed

Heading into January 1994 when the Fed began its “let’s give Don his first reason to hate us” tightening cycle, inflation was running at 2.8% — less than even the Fed Funds rate of 3% at the time.

Today, inflation just hit 8.6% and it’s taken three hikes just to get to 1.5% on Fed Funds.

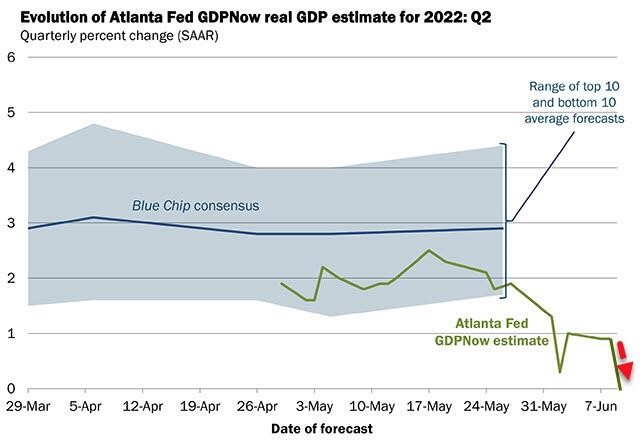

Meanwhile, the Atlanta Fed just updated its second quarter GDP estimate, based on their Real GDPNow model, to zero.

So, after the first quarter’s negative 1.4% print, the United States most likely entered a recession before it even got going on its next job killing campaign.

This stagflationary bind — a shrinking economy with high inflation — is, itself, a meal of the FOMCs making.

And the Federal Reserve isn’t the only central bank forced to eat its own cooking.

The European Central Bank, or ECB, is currently enjoying this frightful morsel. It must simultaneously fight inflation by raising rates while also lowering rates by buying loads of crappy Italian bonds that no one seems to want.

Which, when you think about it, makes the meal the ECB is chasing its own tail.

But among all central banks playing puppet master around the world, none must choke down a meal as stomach turning as the one currently in front of the Bank of Japan (BOJ).

Or Growth Does Have Something to Do With It

Like a roast beef sandwich simmered in a plastic bag under the radiator for three months, the BOJ is about to show the world that you really can’t violate the sacred Trilemma of money.

You see, the privilege of managing the supply of money comes at a cost.

You can manage interest rates (“Sovereign Monetary Policy” below), or you can manage the exchange rate, but you can’t manage both. At least not without turning to the dark arts of capital controls.

Inflation is hitting Japan just as hard as anywhere else. But, instead of raising rates, the BOJ chose to spur growth (I mean, they have been trying to create inflation for 30 years now). Meaning, for them, committing to keeping yields on 10-year government bonds below a quarter of a percentage points, or 0.25%.

But no one wants to own a bond when the yield doesn’t come anywhere near to covering inflation. Thus, the BOJ must step in as the buyer of “last resort.”

And step in it did.

Just a few days ago the BOJ bought 1.5 trillion-yen worth of bonds to defend its rates.

That’s a lot of zeros. But to put that in perspective, the Fed only ever exceed that pace immediately after COVID hit.

In other words, they are buying a lot of bonds. There is no indication they intend to stop buying bonds. In fact, they may well buy up the entire Japanese government bond market before they are through, to defend their ideology. Along the way, the streets get flooded with the Yen printed to pay for those bonds. And, to solve for the inviolable Trilemma, the Yen could go down in history as the first major currency in the age of Full Fiat to go supernova.

I bet those burn going down.

Anyhow, with that row hoed, who knows what comes next. But as one analyst put it you can expect “dramatic, unpredictable non-linearities.”

Or, as I would say it, “try to buck Nature and you’ll find she bucks back.”

The Fed, ECB, BOJ, BOE — all these institutions are committed to a single ideal — suppress the nature of markets. Unfortunately, just like suppressing Nature herself, markets eventually end up doing what they want.

The cost of making either Nature or markets wait to get what they want is more devastation.

Given all the bucking we can expect in markets from not only a “Super Nova” BOJ but also a “behind the curve Fed” and a “tail-chasing” ECB facing us, there’s enormous opportunity in getting your trading on the side of the markets now.

And, on Friday, I’ll show you a way to watch both Nature and markets respond to dramatic, unpredictable non-linearities.

Take What the Markets Give You

PS> On Tuesday I shared my short Yen bet on the BOJs Trilemma with my trading group. Anyone can with a brokerage account can put it on.

But if you find you want the what, how, why, and when of the trade – or just want to make trading market non-linearities a habit – you are free to join my Telegram group any time you’d like.