It seemed easy at the time.

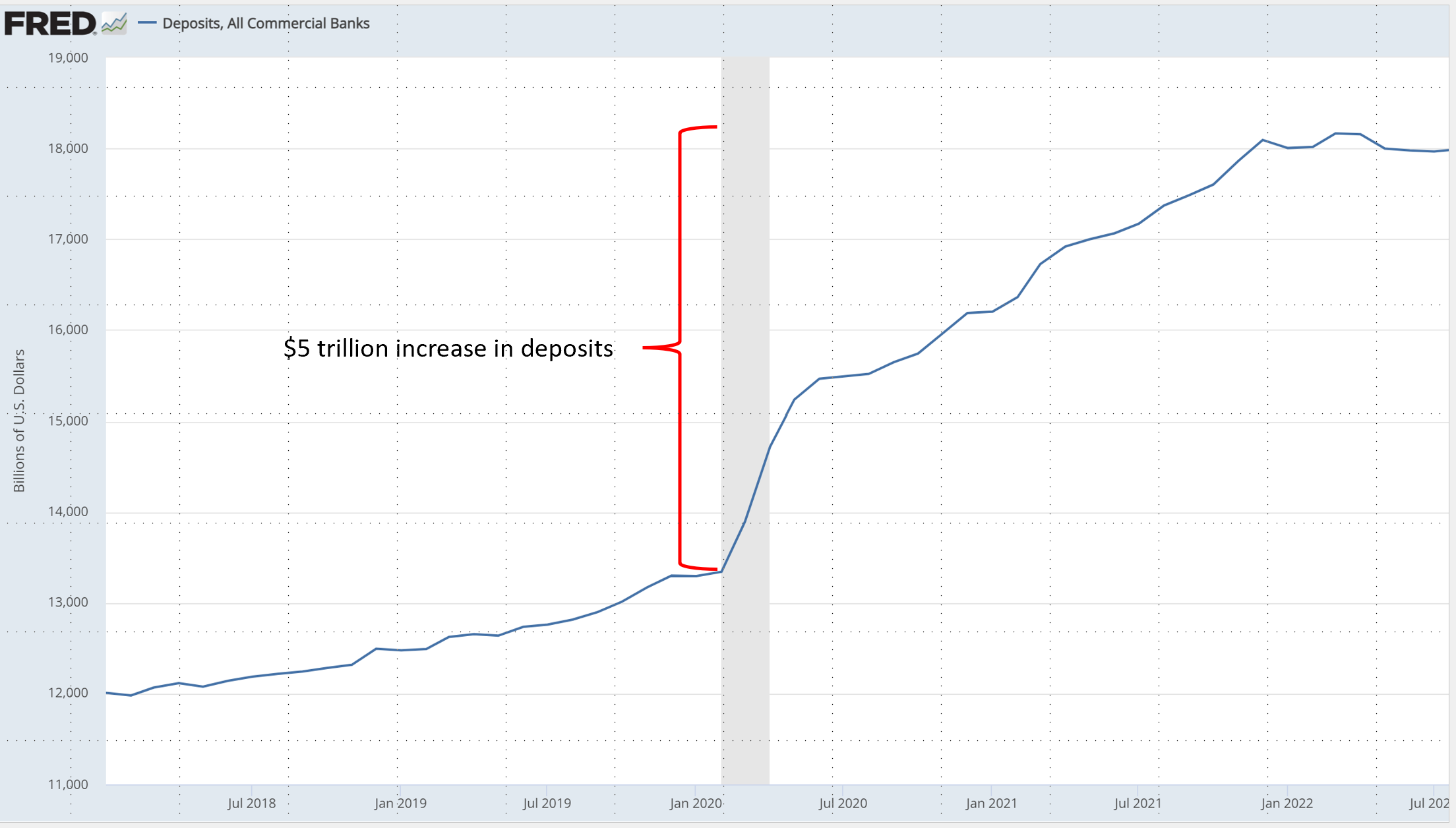

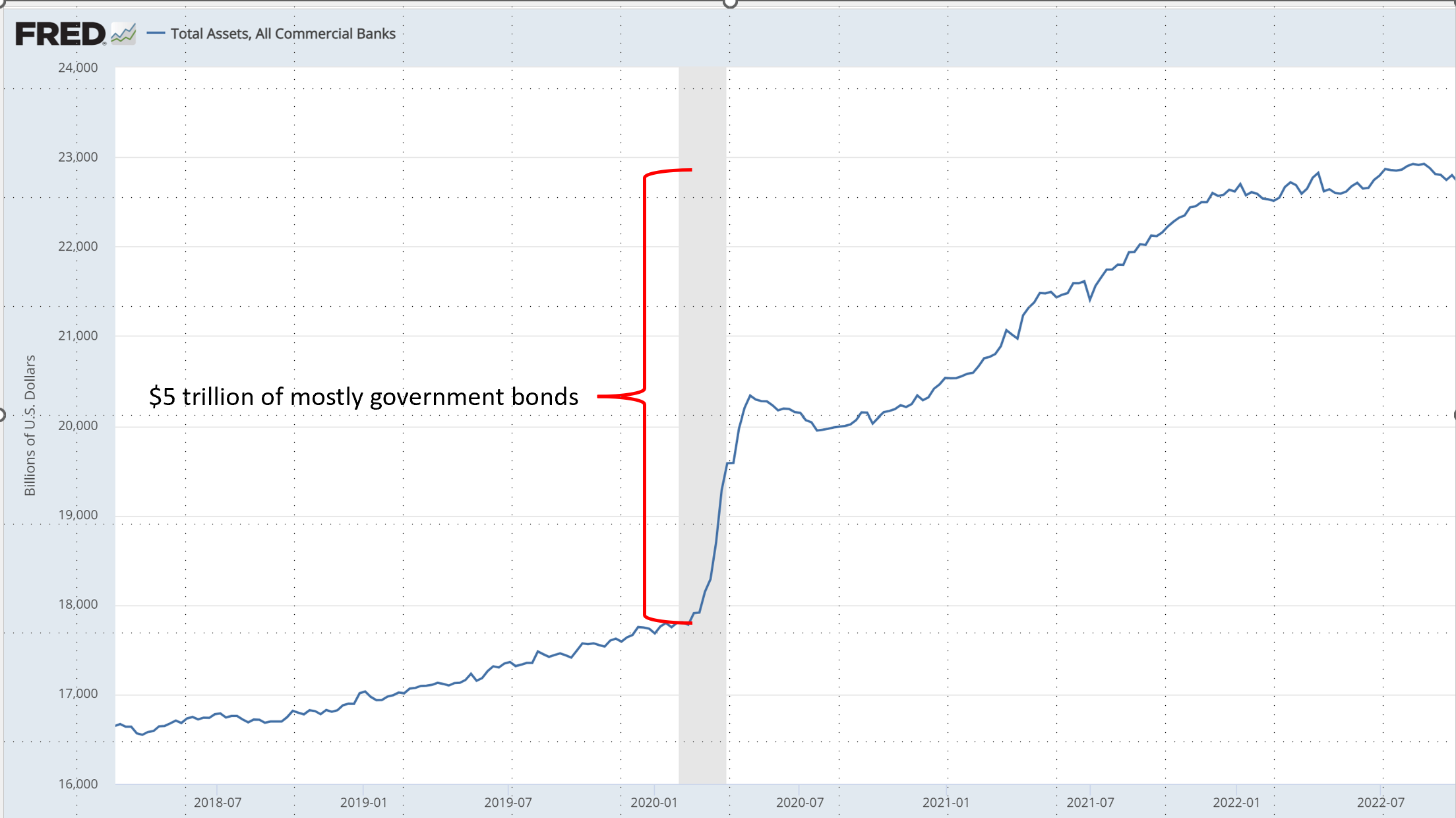

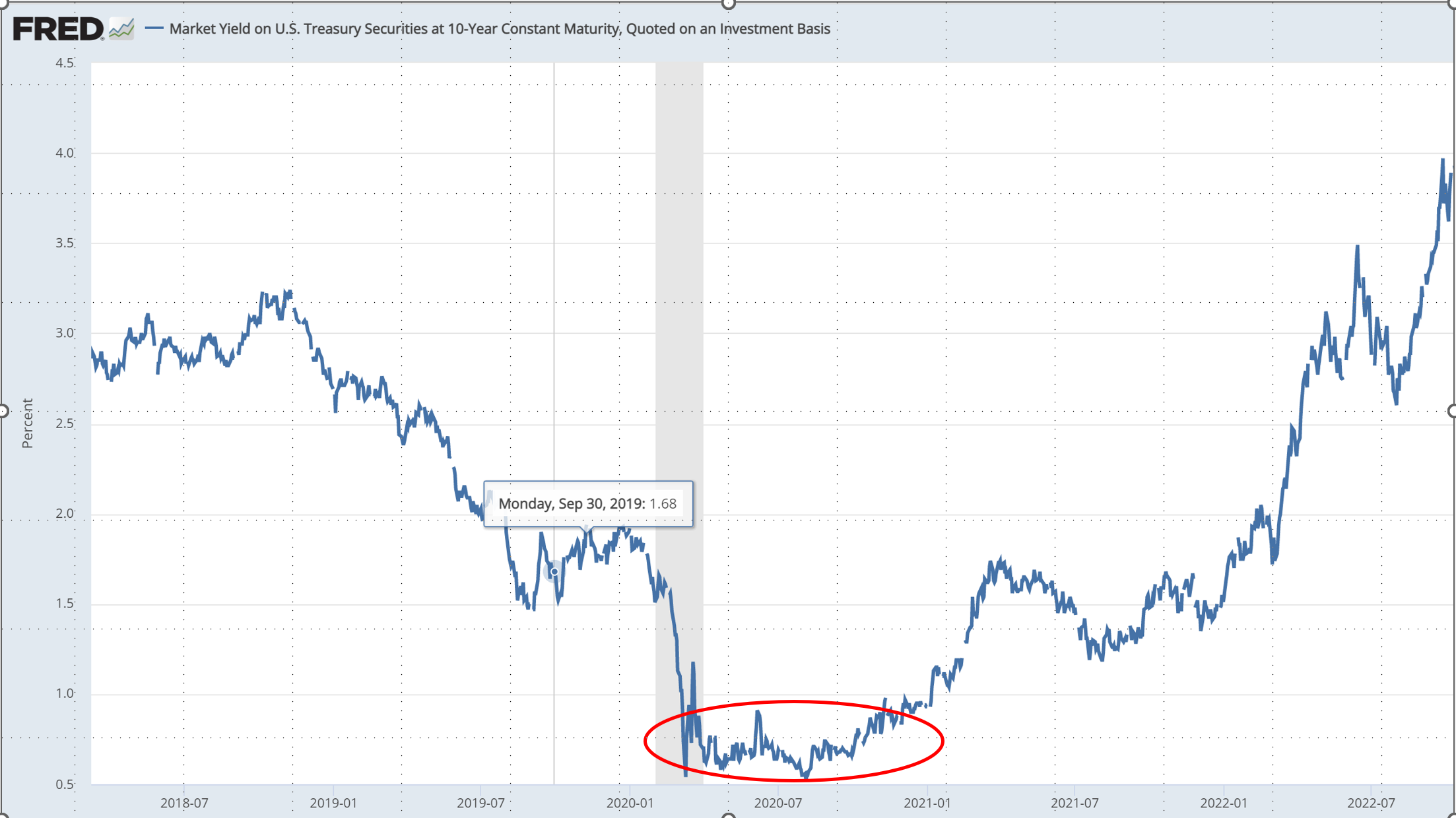

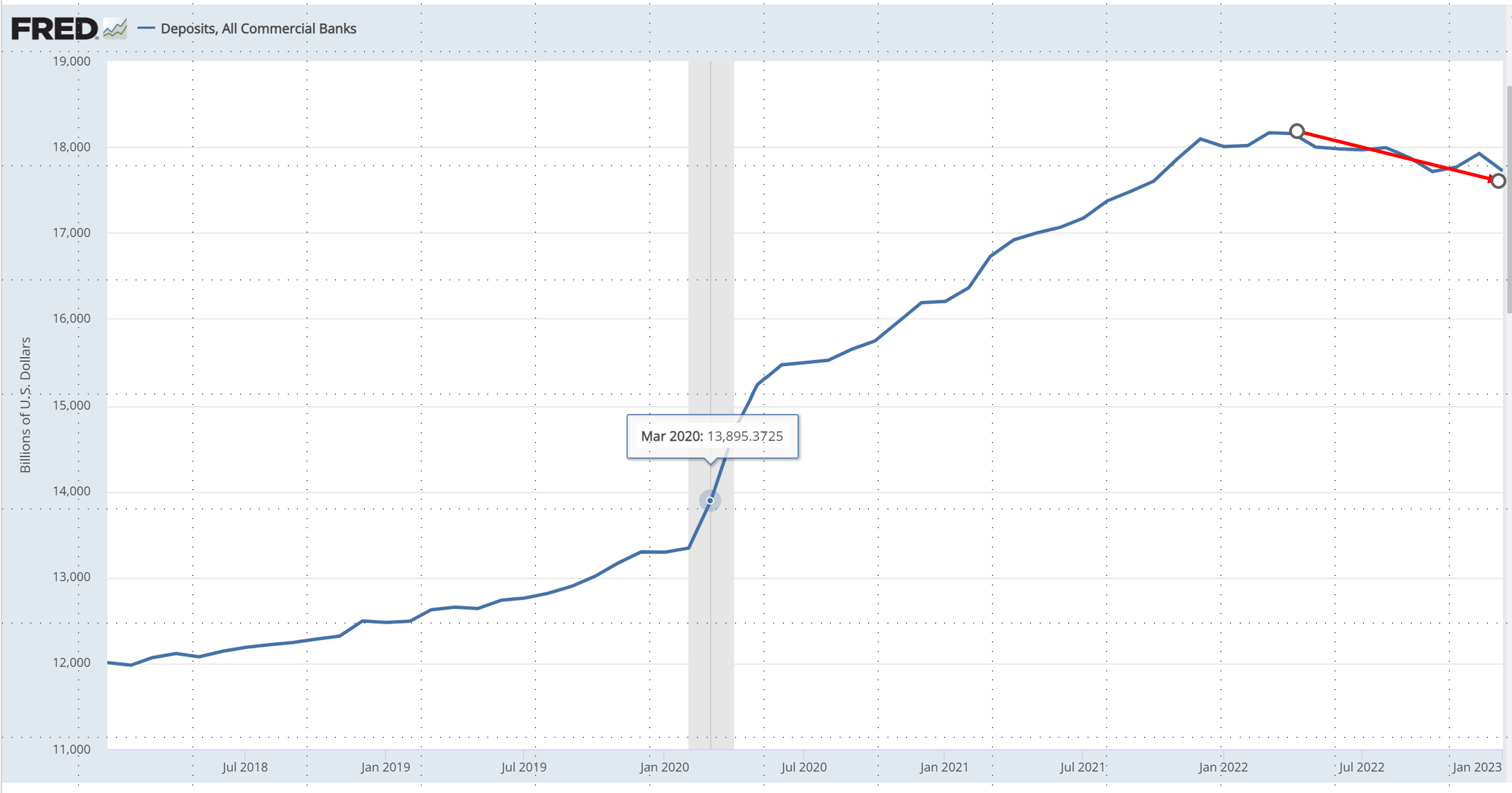

Cheaper than free deposits pour in by the trillions. Use those deposits to buy “risk-free” treasury bonds by the trillions. And despite bond yields at a scant 60 basis points (0.60%), a little yield on deposits that cost banks nothing to keep makes for a lot of profit.

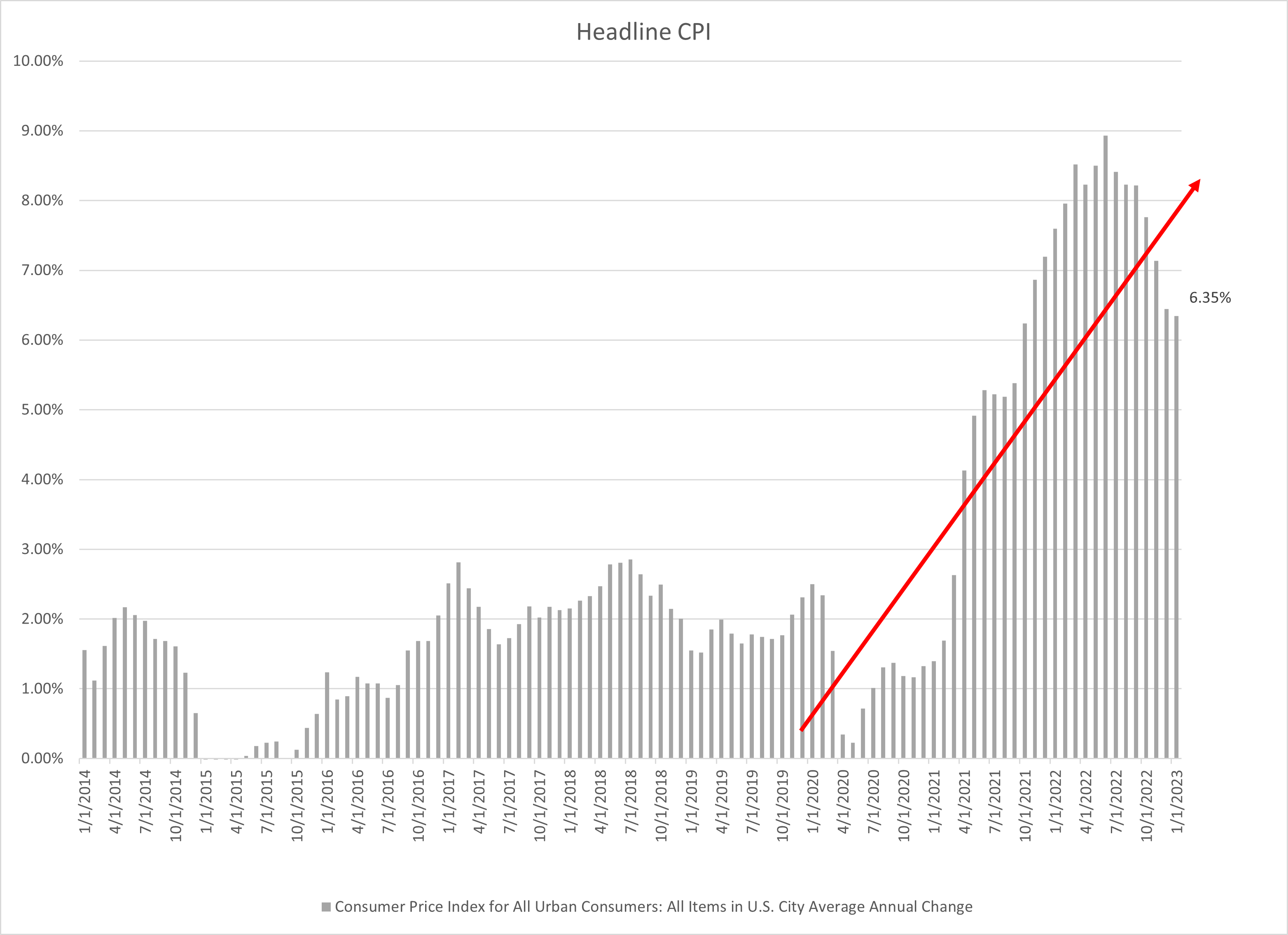

The COVID crisis created boom times for banks.

All those forgivable government-funded business loans and direct stimulus checks flooded banks with deposits. Deposits easily invested in treasury bonds that were issued to fund those loans and stimmy checks in the first place.

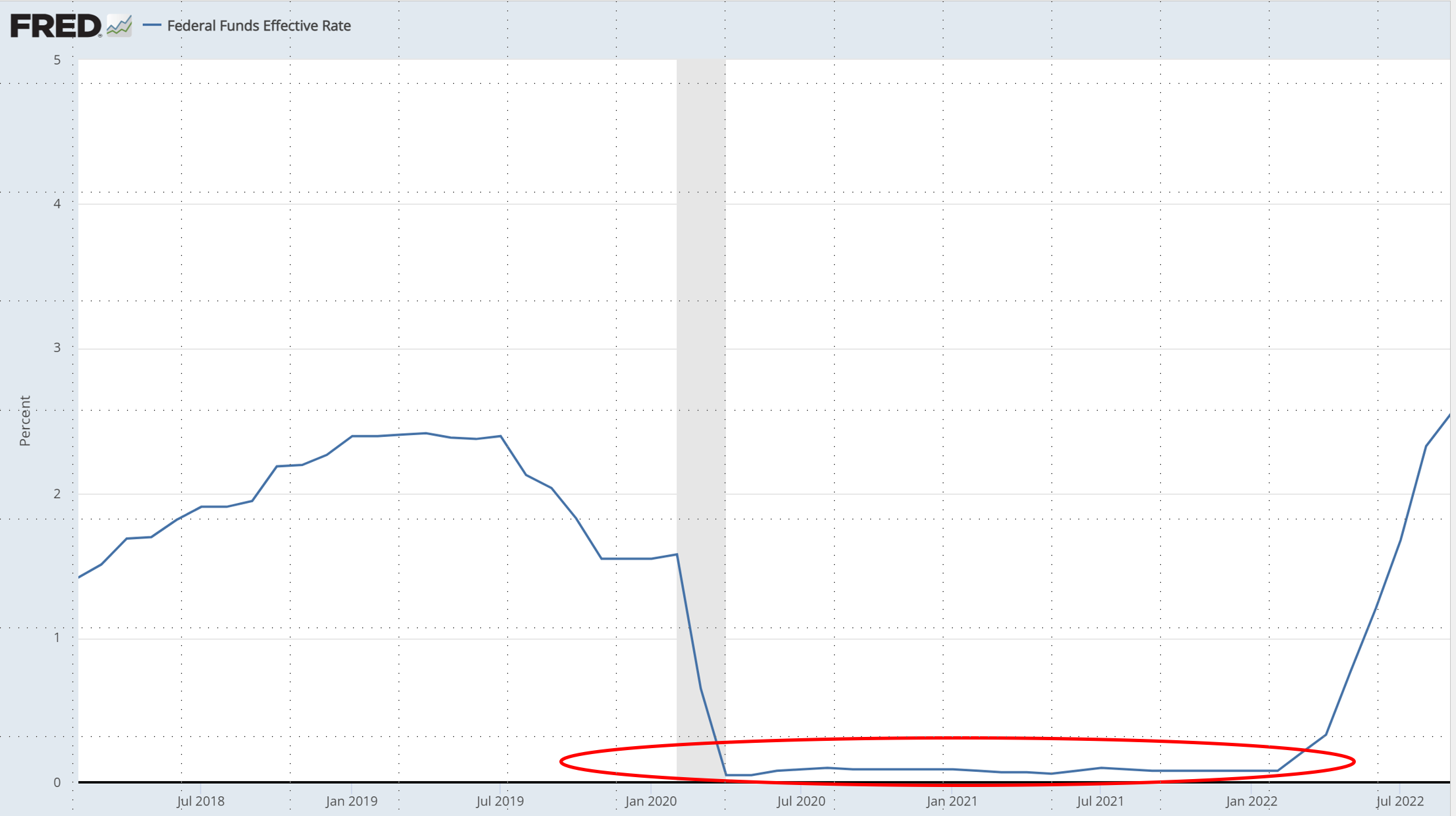

But free money led to inflation. That forced the Federal Reserve to raise deposit rates. Bond yields rose as a result and, of course, their price fell.

Unfortunately, with deposits heading out the door, banks are forced to sell those bonds at a loss.

And everyone is getting reminded that “risk-free” on the way up can mean “risky” on the way down.

Thin Ice

This week, Silvergate Capital (SI) and Silicon Valley Bank faced what was effectively a run on deposits.

And these banks are now selling bonds a la the dynamic I referenced above.

Now, losses on bond portfolios don’t usually spell trouble for banks under normal conditions. Provided bonds are held to maturity, it’s really hard to lose money on treasury bonds because the U.S. government is unlikely to default.

Regulators let banks ignore the losses (i.e., treat the losses as unrealized) because banks can expect to get paid in full.

Sell those bonds when the price is down, however, and mark-to-market losses eat into the bank’s equity. And given that bank equity typically runs at about 10% of bank assets, equity can get wiped out pretty quick. All it takes is a 10% drop in bond prices to wipe a bank’s equity ledger clean.

Since peaking in September, 2020, 10-year treasury prices have since dropped 20% due to both rising inflation expectations and the Fed hiking rates.

That doesn’t mean that all banks have seen similar drops in the value of their assets. But that dramatic drop in 10-year treasury prices does give you a sense of just how thin the ice is getting.

For banks that have lost significant asset value it’s not a problem. At least so long as deposits stay put.

But therein lies the problem.

Bank depositors, investors, and clients now have a lot of reasons to look closely at unrealized losses on bank balance sheets. At the very least we can expect deposits to shift. And the problems created by deposits moving out of weaker banks will outweigh the benefit of deposits flowing into stronger banks.

I’ve mentioned more than a few times the current fragility of markets and the economy. I’ve stated that while it’s hard to predict exactly what will break first, it’s certain that something will break.

I think it just did.

As I said here, here, here, and here, when it breaks, the markets have a long way to fall.

You can’t just blame COVID, though.

The cheap, abundant money dynamic has been in place since quantitative easing killed risk transmission in 2008. That’s more than enough time for fragilities to build up.

But don’t take my word for it. The Federal Reserve just admitted as much.

And with so much fragility in the system, what was easy for the banks on the way up will be hard for everyone on the way down.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}