In 2010, in an attempt to help shore up confidence in the banking system and avoid a repeat of the causes of the Great Financial Crisis, The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 mandated bank stress tests, also known as Comprehensive Capital Analysis and Review (CCAR) and Dodd-Frank Act Stress Tests (DFAST).

These stress tests were designed to assess the ability of large banks to withstand economic stress and financial shocks, such as a severe recession or a sharp decline in asset prices.

They were to be run every year in the hopes of revealing the banks’ capital adequacy, internal controls, risk management practices, and overall financial health.

To do this, the Fed created hypothetical scenarios that simulate adverse economic conditions, such as high unemployment, falling home prices, and a sharp decline in GDP. The scenarios also incorporate factors such as changes in interest rates, exchange rates, and commodity prices.

But as it turns out, the Fed didn’t really simulate anything.

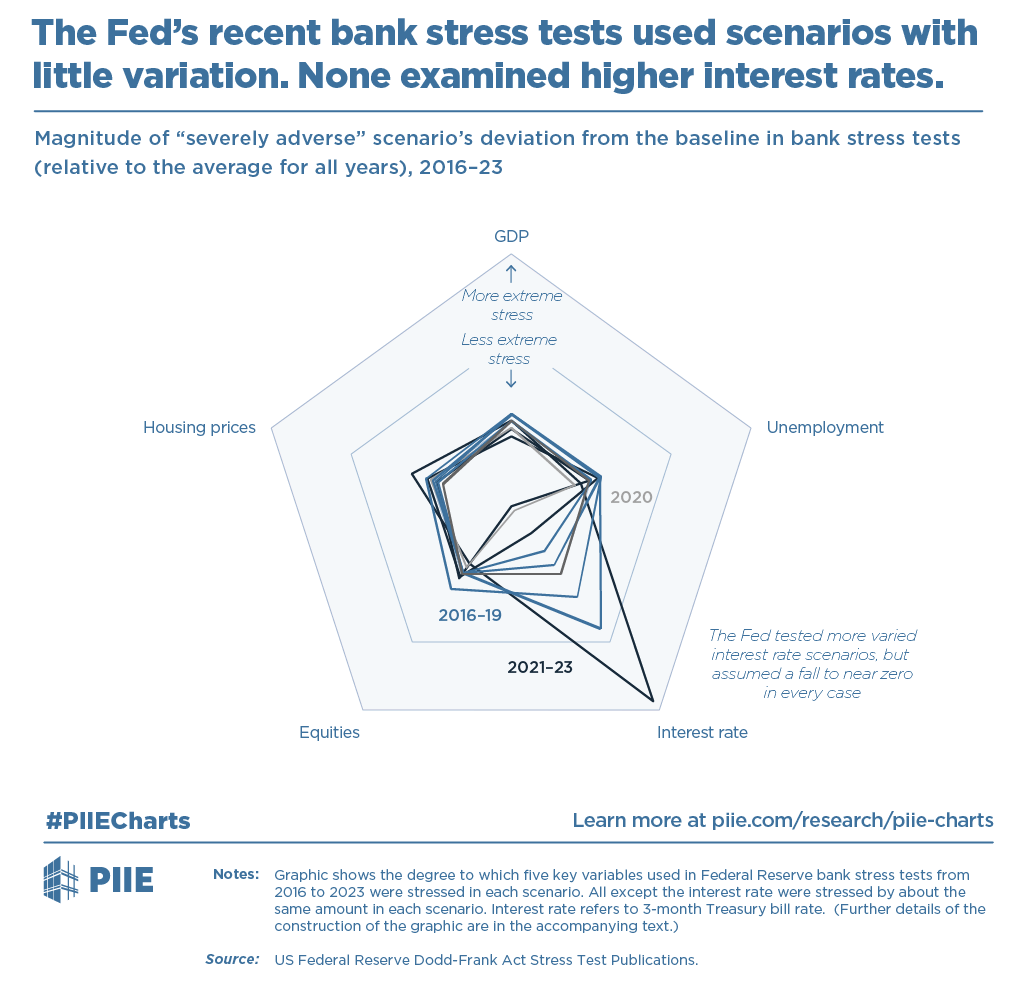

The chart below, (don’t worry,I’ll walk you through it), shows just how much the Fed wiggled 5 of the most significant parameters included in the stress tests since the government stepped in thirteen years ago to help the situation.

The farther a line shoots out from the center, the more the Fed wiggled that parameter.

According to this analysis, the Fed tested the banks ability to withstand large moves in equities, housing prices, GDP, and unemployment by, well… assuming they wouldn’t move.

Each of these four parameters remained well within the “less stress” zone in every single stress test of the past twelve years.

Only short-term interest rates got any heat. But since the Fed knows that the Fed has full control over short-term rates, the Fed always assumed those rates would quickly fall back to zero.

Therefore, they didn’t really wiggle interest rates either.

You know, I always laughed whenever I heard someone cite the results of these stress tests as evidence of the soundness of our banking system.

I knew from the very beginning that these tests were nothing but another tool to mask the zombified, limping, fragile financial monster the Fed created with zero-percent rates and quantitative easing.

Turns out I was right to laugh.

Because it’s not as though the Fed never thought to test the banking system’s ability to withstand the effect higher for longer interest rates would have on bank bond portfolios – i.e, the exact problem stressing the banking system today.

They absolutely knew how much banks would suffer under a sustained rise in long-term interest rates scenario.

They just didn’t want to admit it.

Take What the Markets Give You.