All eyes are on bank earnings coming out next week.

Based on a quick glance of consensus estimates, analysts feel pretty good about big bank prospects, but many smaller regional banks have issues.

There’s a few reasons for this.

First, the “Bigs” have more diversified and recurring revenue streams.

Service fees, large brokerage and asset management businesses, proprietary trading, and commercial banking relationships go way beyond simple checking accounts. This reduces their reliance on the spread they can earn between deposits and loans for profitability.

Regional banks, however, have less revenue tools in the toolbox.

Second, the Bigs also tend to be far more diligent managing interest rate risks. They have the capacity and skills to hedge those risks with sophisticated derivative strategies.

Regional banks often lack the skills to use derivatives effectively. Plus, hedging those risks come at a cost. And, as Round 1 of the bank crisis revealed, many opted to forgo interest rate risk management completely in order to maximize the spread income they earned on the flood of deposits all banks received as a result of Covid stimulus.

So, between having fewer eggs in the basket on the one hand and running carelessly with the basket on the other, analysts expect a long, difficult road ahead for regional banks.

As do their shareholders.

But there’s a more permanent profitability challenge that all banks face. At least until the Federal reserve abandons its inflation fight and cuts short term rates back towards zero.

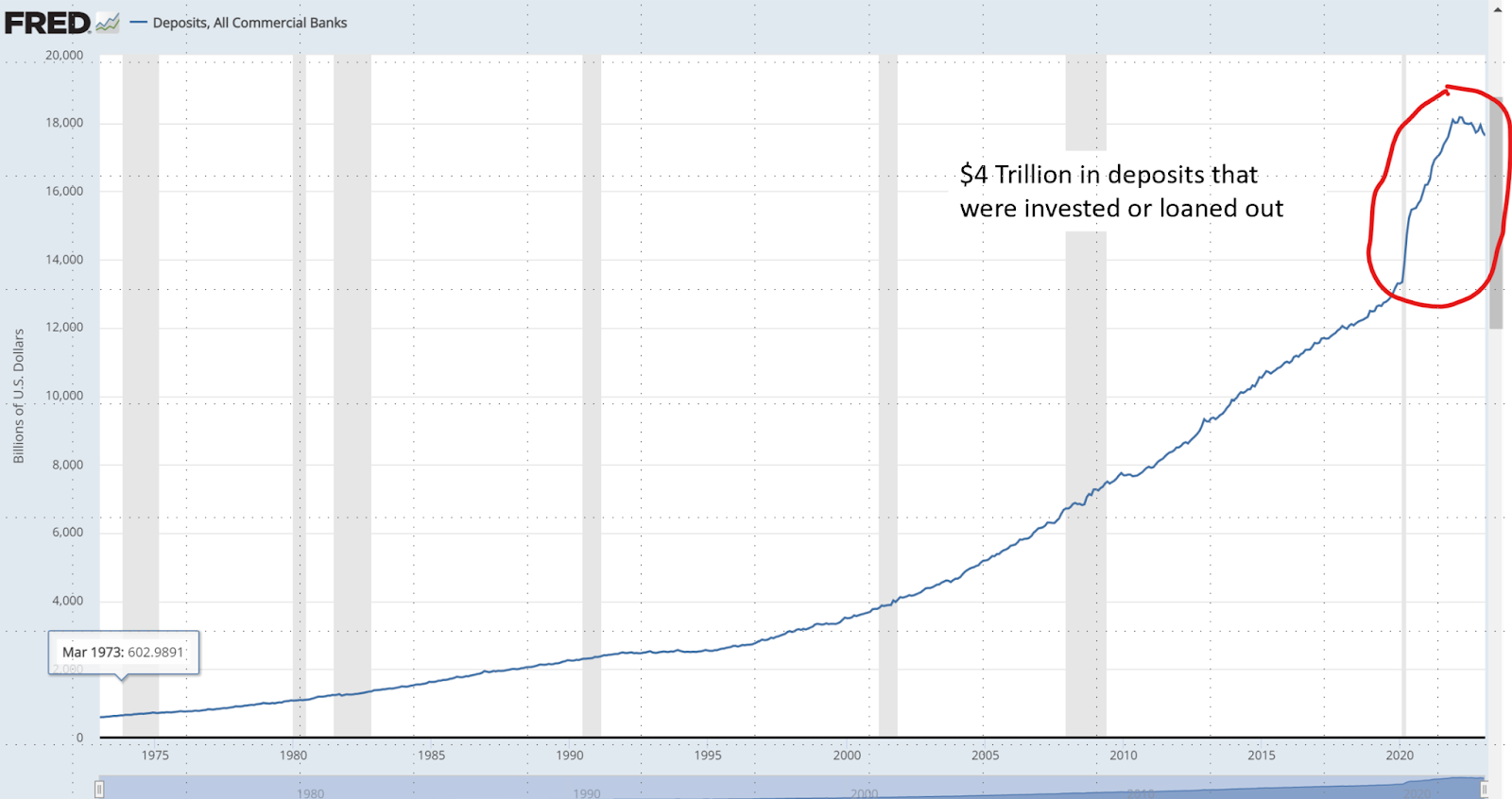

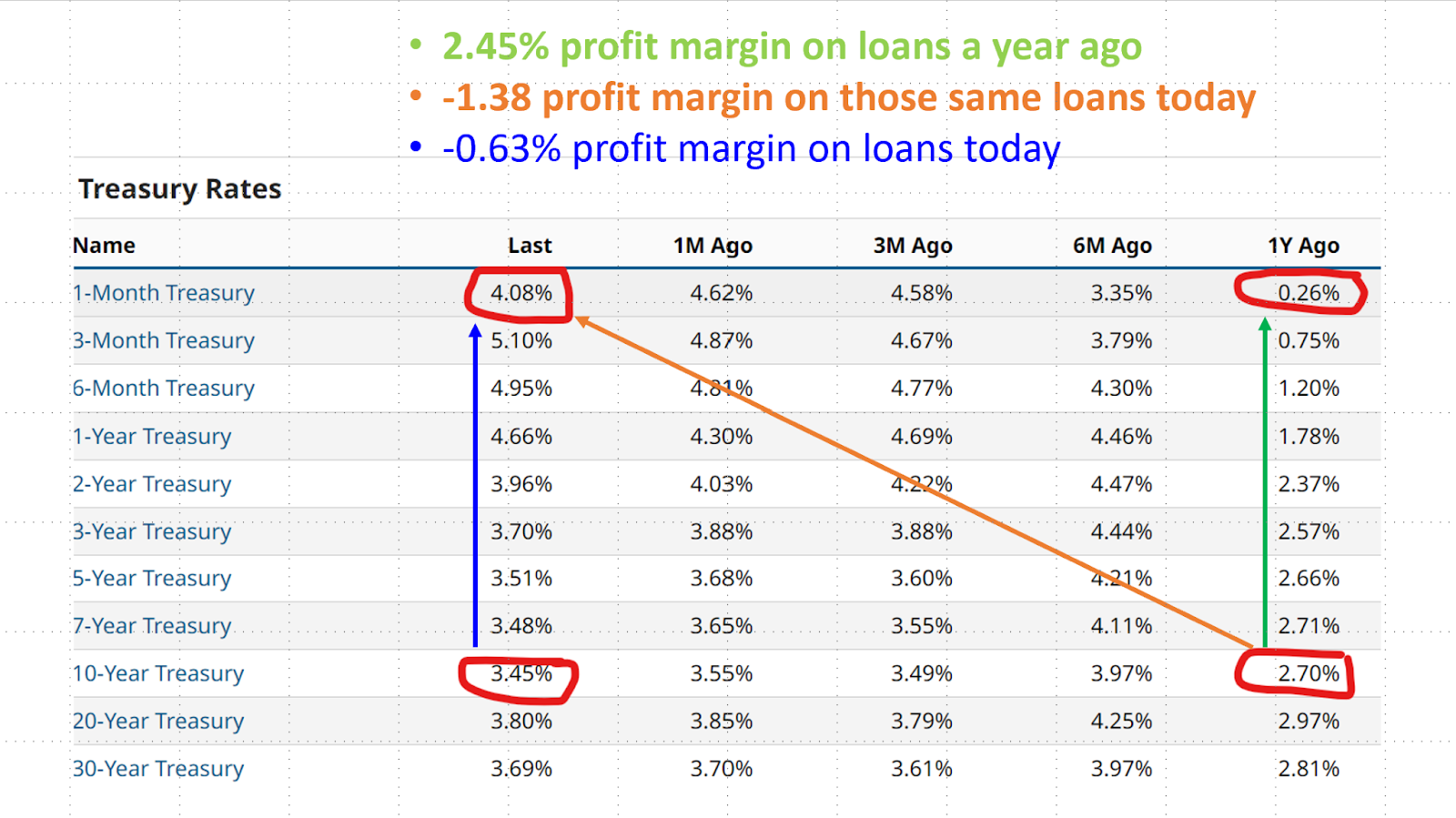

And you can see what I’m talking about in the slide below.

The bottom pair of red circles show 10-year treasury rates. Consider these a proxy for what banks can earn on the loans they make and the bonds they buy.

The top pair of red circles show 1-month treasury rates. These proxy what banks must pay on deposits to continue to fund their loan and bond portfolios.

The column to the far right shows where these rates were a year ago. The column to the far left shows where these rates are today.

One year ago, banks could pay out 0.26% on deposits and use that cash to make loans or buy bonds that yielded 2.70%.

That difference, indicated by the green line in the chart, suggests a profit margin of 2.45%.

But because banks borrow money for such short time horizons (e.g., overnight, monthly, quarterly), they have to continually roll those borrowings over, paying the more current rates.

Today, those short term rates are 4.08% (top left red circle). But the loans and bonds they made a year ago (which they are stuck with) generate income based on the yields from a year ago or before.

The spread, indicated by the orange line, points to a negative spread of 1.28%.

That problem isn’t going away anytime soon.

But the more permanent problem is this.

Banks that don’t raise their deposit rates to current, short-term market rates will lose those deposits.

Assuming they hedged their loan and bond portfolios to offset any losses they suffered on those positions, then the best case scenario is a much smaller deposit base from which they can earn revenue.

Banks that do raise their deposit rates can’t earn enough on loans and bonds to make a profit (the current spread is -0.63% as indicated by the blue line).

In either case, long-term earnings impairment is the best case. And that applies to all banks, regardless of size.

The worst case is permanent asset impairment for those banks that ran carelessly with their basket of eggs.

All the emergency borrowing that banks did directly from the Federal reserve through the discount window delayed that reckoning. Rather than being forced to sell the bonds to meet deposit outflows, they posted the bonds as collateral with the Federal Reserve and received cash to meet deposit withdrawals in exchange.

But that window isn’t a permanent solution. Banks must either raise rates to bring deposits back in the door or sell assets (bonds and loans) at a steep loss (assuming they can be sold).

And for many banks, including the Federal Reserve, the losses on those assets exceed the bank’s equity. Meaning banks, and the Federal Reserve, are technically insolvent.

Think Free. Be Free.