In a note to you earlier today I stated that despite banks folding left and right, “your deposits are completely… totally… most assuredly safe.”

And then claimed that was a bad thing.

Perhaps you thought I was posing a riddle. Maybe you said to yourself, “Ugh… another paradox, Don?”

Well, yes and yes.

But to solve the riddle and resolve the paradox, you need to be clear about what you mean by safety.

If safety means you have $100 in the bank today and, provided you leave it in the bank, you will have $100 in the bank in five years then, yes, it’s safe.

There is no way the U.S. government will allow depositors to lose their money. Their power depends entirely on the masses feeling that the Feds are in control. They will provide blanket insurance for every single penny sitting in banks because 99 out of 100 people have no capacity to see beyond an official assurance placed right at the end of their nose.

A simple change to FDIC policy and their fears will be assuaged.

But if safety means you will be able to buy the same amount of stuff in five years with that $100 as you can today then, well… no, your money isn’t safe at all.

The banking crisis will only get worse and the U.S. government will have no choice but to bail out the entire system.

Whether the federal government swoops in directly and buys up insolvent banks (the fiscal solution) or the Federal Reserve buys up all those underwater bank assets (the monetary solution), the money supply will expand exponentially.

Under the fiscal solution, the U.S. treasury issues debt to buy the bonds and loans sitting on bank balance sheets. But to keep treasury yields from also going exponential, the Federal Reserve will do what it has consistently done since the Great Financial Crises – monetize the federal debt by buying up all the newly issued treasury bonds with newly issued Federal Reserve Notes.

Under the monetary solution, the Federal Reserve buys bank assets directly with newly issued Federal Reserve Notes.

The end result is ultimately the same.

Both use the Federal Reserve’s balance sheet. The only difference will be whether the Federal Reserve holds default-free treasury bonds or lower quality bank assets.

And what do I mean by an “exponential increase in the money supply?”

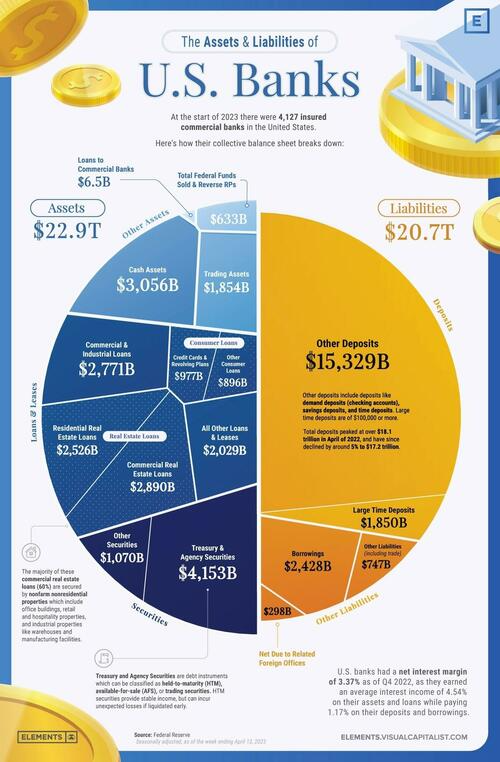

Check out this graphic:

The blue half of the pie chart represents the $22 trillion in assets held by U.S. banks.

Buying those up (yes… I’m suggesting that this is what could be required one way or the other) would require the Federal Reserve to expand the money supply by $22 trillion dollars.

That supply is currently somewhat under $9 trillion. So, we’re talking about a 3-fold leap from current levels and a 39-fold leap from the monetary base just prior to the Great Financial Crisis.

And long before we get to that point, the dollar will be worth much less than it is today.

So, saving your deposits today does not mean your money is safe tomorrow.

Now, I’m not talking about complete and total societal collapse. I’m assuming the wheels of industry and innovation will stay on the economic bus.

What I am saying is that we’re experiencing a transition from one equilibrium to another. And that transition won’t be easy.

We covered this very topic in today’s Ask the Pros.

We also solved another riddle: How do you get a free market anarchist and former federal agent to agree?

Give the latter a profit motive.

Take What the Markets Give You