Yesterday I described the past 50-years in terms of high population growth, globalization, and dollarization.

These factors created a virtuous feedback loop of growth and fiat-backed debt, making the U.S. dollar the supreme Fiat Kingdom. And this kingdom allowed Japan, the U.K., and Europe to build minor kingdoms with the yen, pound, and Euro, respectively.

But the conditions in which these kingdoms emerged don’t describe the future very well. The pro-growth, pro-capital, globalized world of yesterday is giving way to low growth, capital constrained, local markets.

Unfortunately for the kingdoms of fiat, the debt it took to build the world of yesterday is still here today.

Now, had that debt been used to create the productivity required to support it, then debt wouldn’t be a problem. But central banks have abused the dollar-fiat system over the last 20 years. Quantitative easing (QE) flooded the system with currency.

This squeezed the last bits of growth globalization could yield out of the system.

And with every additional debt-backed dollar, yen, euro, or pound yielding less spending bang for the “buck,” it’s now every fiat kingdom for itself…

Abuse of the Absurd Kind

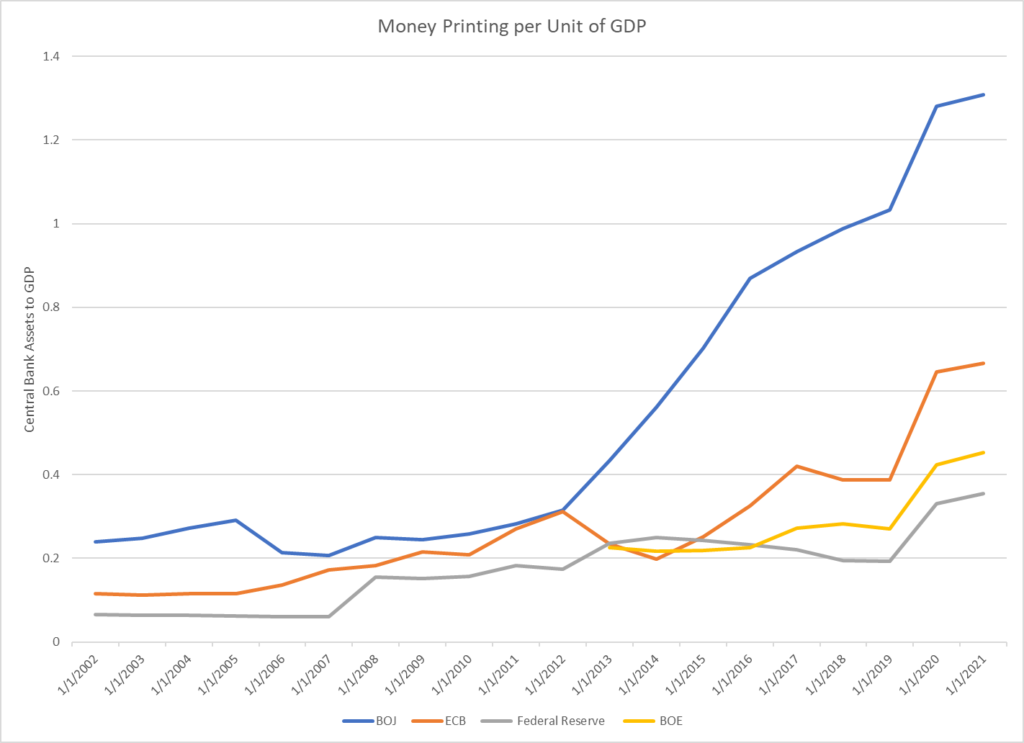

You can see those debt-backed bucks pile up in the form of assets on central bank balance sheets. Compare those respective piles to economic growth and this “declining marginal-productivity of fiat” (sorry…couldn’t resist) clearly emerges.

The chart above shows the ratio of central bank assets to the annual gross domestic product (GDP) of the respective economies in their charge. As currency printing loses effectiveness, that ratio rises. And over the last two decades that effectiveness has collapsed.

So far this century, central bank ineffectiveness has surged across the board by over 5 times. That basket case of basket cases, the Bank of Japan (BOJ), leads the pack with a ratio of 1.3. That means for every yen spent in the Japanese economy, the BOJ printed 1.3 yen to support it.

For a bit of context, these ratios ran between .01 and .05 for decades, or lower than even the lowest point for the Federal Reserve in the above chart. But once the BOJ unleashed QE upon the world in 1998, the abuse of the dollar-fiat system began in earnest and has now reached the inevitable, and absurd, end of the road.

As a result of their precarious peak inefficiency, the BOJ is now simultaneously selling its foreign exchange reserves to buy yen on the open market to prop up the Yen’s value while also selling yen to buy Japanese government bonds to keep interest rates low. It recently teased the market that it would let rates rise – i.e. buy fewer bonds – which ironically forced them to buy more bonds just to keep rates from rising too fast.

They want to break the chains that the impossible trilemma places on money. They will fail.

A sign of that rapidly approaching failure is that the BOJ is now buying bonds (and depleting their foreign-exchange reserve) at such a furious pace that, within a year there will be no more Japanese bonds to buy.

Coming in second in the race to monetary absurdity is the European Central Bank (ECB). It too is simultaneously selling and buying bonds. But for them, the cause of monetary policy failure is the same reason the Eurozone will fail as a political experiment – extreme differences in culture and values.

The ECB wants to sell the European bonds it has spent the last several years buying. But it must keep buying Italian bonds to keep interest rates from reflecting how crappy a credit risk they are.

The BOE – Bank of England – almost bit the bullet first, but their brush with blowing up the UKs fragile pension system resulted in a BOE-led coup that shortened Prime Minister Truss’ term to six weeks.

Plus, they’re all fighting inflation while staring down recession.

Plus, they’re each fighting fiscal policies at home that only increase the cost to fight inflation.

Plus, when one central bank moves on inflation, the other central banks must move further to compensate. They all want to win the Game of Fiat Thrones, and each is willing to push the other off the cliff to do so.

Will Anyone Take the Iron Throne

This century’s surge in central bank ineffectiveness is but a symptom of the low growth, capital constrained world in which we now live.

They kept the Game going as long as they could, and this century delivered fantastic levels of economic growth. But playing it took debt levels 5 times more fantastic to drive it. The population flood that drove the game forward now ebbs. And the underlying economic reality that the current capital base isn’t productive enough to support the debt it took to create it can no longer be avoided.

The kingdoms of fiat will fall. The collapse will start at the top with the BOJ then work its way through the other great houses in order of decreasing ineffectiveness.

And the monetary order that emerges on the other side of this brief (historically speaking) experiment in full-fiat madness is anyone’s guess.

I have mine. What’s yours?

Think Free, Be Free.

P.S. For more macro-economic insights, join me and other like-minded traders on my FREE Prosperity Pub Community on Telegram.